Universal Banking in India

- Definition: A ‘cafeteria’ approach offering retail, wholesale, and investment services, acting as a ‘full-service’ bank.

- Recommendations:

- Narasimham Committee (1988)

- Khan Working Group (1998)

- Disadvantage: Loose regulatory norms can derail the entire banking system.

1. Merchant/Investment Banks

- Role:

- Help companies raise funds in the capital market.

- Provide advisory services on mergers and acquisitions.

- Underwrite new public issues floated by companies.

- Deal exclusively with corporates, not with the general public.

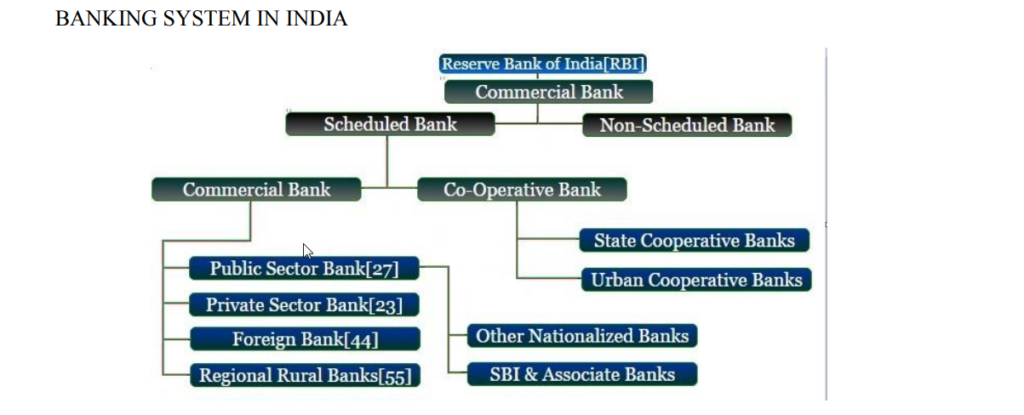

2. Commercial Banks

- Serve as financial intermediaries between depositors and borrowers.

- Cater to short-term working capital requirements.

3. Scheduled Commercial Banks

- Listed in the Second Schedule of the RBI Act, 1934.

- Conditions:

- Paid-up capital and reserves > ₹5 lakh.

- Must satisfy RBI that their operations are not detrimental to depositors.

- Privileges:

- Access to bank rate loans from RBI.

- Clearing house membership.

- Ability to rediscount exchange bills with RBI.

- Obligations: Maintain required reserves.

4. Non-Scheduled Banks

- Not listed in the Second Schedule of the RBI Act, 1934.

- Key Features:

- No access to privileges available to scheduled banks.

- Required to maintain CRR, but can keep it with themselves.

- Includes:

- Local Area Banks (LABs).

- Foreign banks without branches in India.

- Some Urban Cooperative Banks (UCBs).

- Restrictions:

- Limited branch expansion.

- No loans from RBI via bank rate or Marginal Standing Facility (MSF).

- No refinance from NABARD or SIDBI.

Differentiated Banking

- Introduced based on recommendations of the Nachiket Mor Committee (2013).

Differentiated Banking

- Definition: Banks that offer limited services and operate in niche segments.

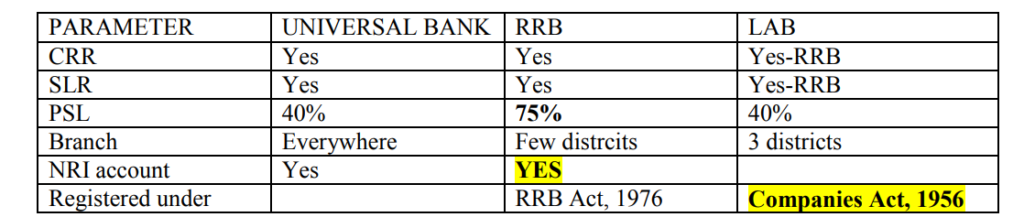

A. Regional Rural Banks (RRBs)

- Established: Under RRB Act, 1976, confined to specific regions.

- Regulator: NABARD.

- Development:

- In 1997, allowed to lend outside target groups.

- Owned by:

- Centre: 50%.

- State: 15%.

- Sponsor Bank: 35%.

- Amendment (2015): Allowed 49% private investment, but 51% ownership remains with Centre + State + Sponsor Bank.

- Key Features:

- Priority Sector Lending (PSL): 75%.

- Not eligible for Marginal Standing Facility (MSF) or Liquidity Adjustment Facility (LAF) as their interest rates are regulated by RBI.

B. Local Area Banks (LABs)

- Established: 1996.

- Unique Feature: Only type of Non-Scheduled Banks in India, though eligible for inclusion in the Second Schedule.

- Objective: Operate in rural and semi-urban areas to promote financial inclusion in backward and less developed districts.

- Operational Scope:

- Geographical restriction to three contiguous districts, with only one urban center per district.

- Regulatory Details:

- Registered under the Companies Act, 1956.

- Licensed under the Banking Regulation Act, 1949.

- Regulated by RBI (not NABARD).

- Capital and Lending:

- Minimum Capital: ₹5 crore.

- PSL Requirement: 40% (at least 25% for weaker sections).

Comparison Between Small Finance Banks (SFBs) and Payment Banks (PyBs)

Similarities

- Regulatory Compliance:

- CRR and SLR: Both maintain Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR).

- Payment Banks: SLR consists of 75% in G-Secs + 25% in Scheduled Commercial Banks (SCBs).

- FDI Limit:

- 49% under the automatic route, up to 74% with approval.

- Repo Market Participation:

- Both can participate.

- Services:

- Allowed to operate ATMs, appoint Business Correspondents (BCs), open branches, and issue debit cards.

- Can sell Mutual Funds (MFs), pension schemes, insurance, and forex services but cannot use their own funds for these purposes.

- Branch Requirement:

- At least 25% of branches must be in rural areas.

Differences

| Parameter | Small Finance Banks (SFBs) | Payment Banks (PyBs) |

|---|---|---|

| Client Base | Focuses on unserved and underserved customers like small and marginal farmers, micro and small industries. | Targets small savings, remittances for migrant labor families, low-income households, unorganized sectors, and small businesses. |

| Deposit Features | No limits on deposits. | 1. Cannot accept NRI deposits. 2. Accepts both time and demand deposits. 3. Maximum balance per customer: ₹1 lakh/year. 4. Cannot issue credit cards. |

| Priority Sector Lending (PSL) | – 40% PSL as per commercial bank norms. – 35% additional PSL as per their niche focus (total: 75% PSL). | 1. Not applicable (as they do not give loans). 2. Must maintain 75% demand deposits in G-Secs or T-bills; maximum 25% can be placed with SCBs. |

| Future Scope | Can evolve into Universal Banks after 5 years of operation. | In 2019, RBI permitted Payment Banks with 5 years of experience to apply for conversion into Small Finance Banks. |

| Call Money Market | Not explicitly mentioned. | Now allowed to participate in the Call Money Market as both borrower and lender. |

Note:

Payment Banks focus on promoting financial inclusion, especially for low-income groups, while Small Finance Banks aim to address broader credit and deposit needs of underserved segments.

C. Small Finance Banks (SFB)

- RRR committee, 2009

- Cannot: Large loans, set subsidiary to undertake non-banking financial service activities.

- Who are eligible: NBFCs, MFIs, LABs, individuals with 10 years of experience in finance.

D. Payment Banks

- Accept restricted deposit: ₹1,00,000.

- FDI is allowed, at least 26% investment of Indians.

- Can: Services like ATM, debit card, net banking.

- Can NOT: Lend, credit card, NRI deposits, cross-border remittance, cannot form subsidiary to undertake non-banking activities.

INDIA POST PAYMENT BANK (IPPB)

- T.S.R. Subramaniyam committee on postal network.

- Companies Act, 2013.

- 100% Equity of DoPost (under MoCommunication).

- Who can open account:

- Age: >10 years.

- Zero balance a/c.

- Also, current a/cs with post can be transferred to IPPB.

- Initially: 1 post in each district (having license) >>> later ALL.

- 3 types of accounts:

- SAFAL

- Sugam

- SARAL

- NO ATM, but QR-based biometric cards.

E. Wholesale and Long Term Finance (WTLF) Banks

- Only current account.

- Fixed or Term deposits only above ₹10 crore.

- Lending to:

- Infra projects.

- Small, medium, corporate business.

- Help PSL targets for banks (through PSL Certificates).

7. COOPERATIVE BANKS

| PARAMETER | COMMERCIAL BANKS | COOPERATIVE BANKS |

|---|---|---|

| Banking Regulation Act | Yes (Regulated by RBI) | Yes (from 1966) (Regulated by RBI) |

| CRR and SLR | Yes | Yes |

| MSF, PSL | Yes | UCB – 40% (+10% – minority + 7.5% – micro enterprises) |

| Who can borrow | Anyone | Only members |

| Vote power | Shareholding | 1 person 1 vote |

| Profit motive | Yes | No profit, No loss |

| Presence | All India, Abroad | GJ, MH, AP |

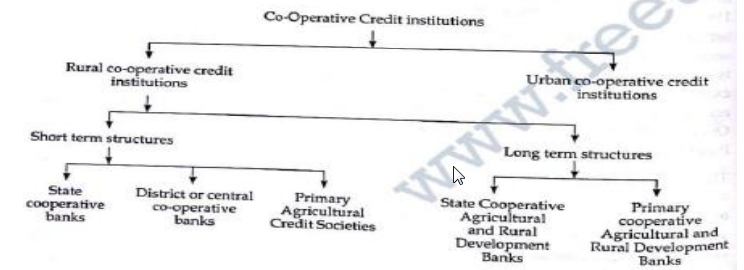

- Set up: By either State (Cooperative Acts) or Central law (Multistate Cooperative Societies).

- Regulation: Governed by the Banking Regulation Act, 1949, and the Banking Laws (Cooperative Societies) Act, 1965.

- Urban Cooperative Banks (UCB):

- Divided into Scheduled and Non-Scheduled categories.

- Regulated by the RBI.

- Deposits covered by DICGC up to ₹5 lakh.

- Rural Cooperative Banks (RCB):

- Regulated jointly by NABARD (ultimately under RBI).

- Financial and Other Assistance: Provided by RBI, the Central Government, State Governments, and NABARD.

- Hierarchy: State Cooperatives → District Banks (DCC) → Rural Cooperatives.

- 2017: The government allocated funds to NABARD for implementing Core Banking Solutions (CBS) between Rural and District Cooperatives.

NON-BANKING FINANCIAL INSTITUTIONS

Development Financial Institutions (DFIs)

- Definition: Institutions providing long-term finance for industries.

- Key DFIs:

- IDBI

- ICICI

- IFCI

- Changes Over Time:

- 1991: DFIs abolished based on recommendations of the Narasimham Committee; AIFIs replaced DFIs.

- 2020: The Finance Minister announced the establishment of Development Banks to provide long-term credit for capital-intensive investments.

1. ALL INDIA FINANCIAL INSTITUTIONS (AIFIs)

- Regulated by: RBI.

| Parameter | EXIM | NABARD | NHB | SIDBI |

|---|---|---|---|---|

| Year | 1982 | 1982 | 1988 | 1990 |

| Role | Loan/credit/finance to exporters and importers | 1. Rural Infra Dev Fund (RIFD): banks deposit PSL shortfalls 2. Indirect refinancing for farmers | 1. Finance banks and NBFCs for housing projects 2. RESIDEX | 1. Small Enterprises Devlopment Fund (SEDF): PSL shortfalls of foreign banks with <20 branches deposited here |

| Boss | GoI (100%) | Earlier: 99.3% GoI + 0.7% RBI 2019: GoI (100%) | Earlier: RBI 2019: GoI (100%) | SBI + LIC + IDBI + other PSBs + Insurance companies |

| Regulatory Authority | RRBs + Cooperative Banks | Apex institution for housing finance |

PRIMARY DEALERS

- Role: Operate in the “primary” market, directly buying G-Secs during RBI’s E-Kuber auctions and selling them in the secondary market.

- Participation: Eligible to participate in Open Market Operations (OMO).

- Licensing: Requires a license from RBI.

- Total Primary Dealers: 21 (14 banks + 7 non-bank entities).

NON-BANKING FINANCIAL COMPANIES (NBFCs)

- Definition: Engaged in activities like loans, advances, housing finance, and securities acquisition, but their principal business does not include agricultural, industrial, or immovable property activities.

Differences Between Banks and NBFCs:

| Parameter | Banks | NBFCs |

|---|---|---|

| Registration | Banking Regulation Act | Companies Act, 1956 |

| Entry Capital | ₹500 crore | ₹5 crore for microfinance, ₹2 crore for others, ₹200 crore for reinsurers |

| Supervision | RBI | Various regulators |

| Deposits | Time and Demand Deposits | Only Time Deposits (NBFC-D) |

| Chequebook | Allowed (Payment Settlement Act, 2007) | Not Allowed |

| Reserve Ratio | CRR and SLR | No CRR; SLR applicable only for NBFC-D |

| Investment | Cannot invest in share markets | Can invest in share markets |

| Loan Rate | MCLR | Variable |

| Loan Recovery (SARFAESI) | Yes | Only for housing finance |

NBFC Categories

- NBFC-ICC (Investment and Credit Company): Merger of Asset Finance Companies (AFCs), Investment Companies, and Loan Companies.

- Mutual Benefit Financial Company (MBFCs): Cooperative financial institutions.

- NBFC-Factor: Specializes in receivables factoring.

Classification by Deposits

- NBFC-D: Accepts deposits but not NRI deposits, except those debited from NRO accounts.

- NBFC-ND: Non-deposit-taking NBFCs.

Systematically Important Non-Deposit Core Investment Company (CIC-ND-SI):

- Definition:

- Asset size > ₹100 crore.

- Holds ≥90% of its net assets in equity shares, preference shares, bonds, debentures, or loans in group companies.

- Accepts public funds.

- Regulated by RBI.

Notes:

- Housing Finance Companies, Merchant Banking Companies, Stock Exchanges, Venture Capital Fund Companies, Nidhi Companies, Insurance Companies, and Chit Fund Companies are all categorized as NBFCs.

MUDRA BANK

- Registration: Registered as an NBFC-ND and established as a subsidiary of SIDBI.

- Initial Role: Initially proposed as a regulator for MFIs but later assigned to RBI and the Department of Company Affairs.

- Purpose: Provides refinancing to all banks under the Pradhan Mantri Mudra Yojana (PMMY).

- Responsibilities:

- Develop a robust credit delivery architecture for micro-businesses under PMMY.

- Prioritize enterprises led by SC/ST, first-generation entrepreneurs, and existing small businesses.

Pradhan Mantri Mudra Yojana (PMMY)

- Objective: To provide funding to the Non-Corporate Small Business Segment (NCSBS).

- Loan Coverage: Up to ₹10 lakh for non-corporate, non-farm micro and small enterprises.

- Loan Providers:

- Commercial Banks (including foreign banks).

- RRBs.

- SFBs.

- Cooperative Banks.

- MFIs.

- NBFCs.

- Loan Categories:

- Shishu: Up to ₹50,000; no collateral; 1% interest for 5 years.

- Kishor: Up to ₹5,00,000.

- Tarun: Up to ₹10,00,000.

- Implementation: Handled by the Department of Financial Services (also responsible for PMJDY, Atal Pension Yojana, PM Jeevan Jyoti Bima Yojana, and Suraksha Bima Yojana).

SHADOW BANKS

- Definition: Operate similarly to banks but are not subject to stringent regulations, leading to less transparency.

- Characteristics:

- Higher cost of funding, greater risk-taking, and higher returns.

- Not deposit-taking institutions; cannot create money.

- Liabilities are not insured and have no access to RBI’s liquidity.

- Examples: NBFCs, Chit Funds.

VARIOUS COMMITTEES

1. Narasimham Committee (1991 and 1998)

Recommendations (1991):

- Stop further nationalization of banks.

- Reduce SLR and CRR.

- Ensure a level playing field for public, private, and foreign banks.

- Identify select banks for global operations.

- Deregulate interest rates.

- Set up Asset Reconstruction Companies (ARCs) for bad loans.

- Introduce prudential norms for risk management.

- Rationalize and better target Priority Sector Lending (PSL).

2. P. J. Nayak Committee

- Purpose: Review governance of bank boards (public and private).

- Recommendations:

- Repeal Bank Nationalization Acts (1970, 1980) and SBI Act.

- Establish a Bank Investment Company (BIC):

- Formed under the Companies Act, 2013, as a ‘core investment company.’

- Transfer PSB shares to BIC and make banks its subsidiaries.

- Rationale: BIC would have voting power to appoint bank Boards of Directors and grant autonomy to banks.

- Bank Appointments in PSBs:

- Phase I: Bank Boards Bureau (BBB) to oversee appointments.

- Phase II: BIC to manage the process.

- Phase III: Grant appointment powers to PSB boards.

- Set fixed tenures:

- 5 years for Chairpersons/MDs.

- 3 years for Whole-time Directors.

BASEL NORMS (Basel Accords)

- Definition: A set of recommendations for the regulation of banks and Systemically Important Financial Institutions (SIFIs).

- Issued by: Basel Committee on Banking Supervision (BCBS).

- Objective: Ensure banks have sufficient capital to meet obligations and absorb unexpected losses.

BASEL III

- Introduction: Rolled out in 2013, with implementation up to 2019.

- Risks Covered:

- Credit Risk: Banks must measure credit risk and maintain sufficient capital.

- Market Risk: Includes risks from market fluctuations (except for government securities).

- Operational Risk: Covers risks like fraud, security breaches, privacy violations, and environmental issues.

Two Components of Basel III:

A. Capital

- Pillars of Capital:

- CRAR: Minimum Capital to Risk-Weighted Asset Ratio (CRAR) of 8%, plus an additional Capital Conservation Buffer of 2.5% for financial stress.

- Counter-Cyclical Capital Buffer: Extra capital during economic booms to prevent unhealthy credit expansion.

- Leverage Ratio: Capital measure / exposure measure (to account for unusual exposures).

- Risk Management and Supervision:

- Banks to implement internal risk assessment processes.

- Central banks to conduct review processes.

- Market Discipline:

- Mandates disclosure of capital adequacy, risk exposure, and risk assessment procedures.

B. Liquidity

- Liquidity Coverage Ratio (LCR):

- Stock of High-Quality Liquid Assets (HQLA) must withstand a liquidity crisis for 30 days.

- Net Stable Funding Ratio (NSFR):

- Ratio of required stable funding to available stable funding, preventing the creation of long-term assets using short-term funding.

CAPITAL ADEQUACY NORMS (CRAR or Capital to Risk-Weighted Asset Ratio)

- Definition: Percentage of a bank’s risk-weighted credit exposure.

- Mandate:

- RBI requires 9% CAR (international norm: 8%).

- G-secs are subtracted from total assets to calculate CAR (since they are risk-free).

- India’s Compliance:

- Indradhanush Scheme: Government recapitalized banks to help meet Basel III norms by March 2019.

- Needed due to low profitability and difficulty in raising equity.

VARIOUS ACTS AND STEPS

1. SARFAESI Act (Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act)

- Applicability: Loans above ₹10 lakh.

- Empowers Banks to:

- Take possession of a borrower’s assets and sell them (2011 amendment allows banks to purchase assets if no buyer is available).

- Change management of those assets.

- Demand surrender of assets already sold to third parties by the borrower.

- Exclusions: Cannot take personal assets or agricultural land.

- Appeal by Borrower:

- To Debt Recovery Tribunal (DRT) (not civil courts).

- If dissatisfied, appeal to Debt Recovery Appellate Tribunal (DRAT) (must deposit 50% of the pending loan).

2. Insolvency and Bankruptcy Code (IBC)

- Who can initiate:

- Financial creditors

- Operational creditors

- Corporate debtor

- Employees

- Shareholders

- Committee of Creditors:

- Composed of financial creditors.

- For smaller firms:

- Fast track Insolvency Resolution Process (IRP) of 90 days, extendable with 75% consent of financial creditors.

- Liquidation Process:

- Administered by an Insolvency Professional (IP).

- Priority in Liquidation:

- Worker salaries for up to 24 months take precedence over secured creditors.

- Jurisdiction:

- NCLT: For Companies and LLPs

- DRT: For Individuals and Partnership Firms

3. Asset Quality Review (AQR)

- 2015-16: Special inspection to ensure asset classification follows prudential norms.

- Impact:

- Banks reclassified stressed assets identified by AQR as Non-Performing Assets (NPA).

4. Prompt Corrective Action (PCA)

- Purpose:

- Allows RBI to impose restrictions on banks when certain risk thresholds are breached.

- Thresholds for PCA:

- Asset Quality: Net NPA

- Profitability: Return on Assets (RoA)

- Capital: CRAR (Capital to Risk Asset Ratio)

- Leverage Ratio: Added as a 4th parameter

- Trigger Points:

- CRAR: 9%

- Net NPA: 10%

- RoA: 0.25%

- Exemptions:

- PCA doesn’t apply to Cooperative Banks, NBFCs, and Financial Market Infrastructure (FMIs).

- For Cooperative Banks: Supervisory Action Framework (SAF) is applicable, akin to PCA.

- Current Banks under PCA:

- Only 6 Public Sector Banks (PSBs).

- Corrective Actions Allowed:

- Halt banking expansion

- Stop dividend payments

- Cap lending limits

- Special audits

- Restructure operations

- Recovery plans

- Bring in new management

- Supersede bank boards

- PCA for RRBs:

- Managed by NABARD (since 2018).

5. Strategic Debt Restructuring (SDR)

- Purpose:

- Change in ownership as part of restructuring of distressed assets.

6. Stress Test

- Purpose:

- Analysis of a bank’s ability to withstand economic or financial crises.

- Conducted by RBI.

7. Asset Reconstruction Company (ARC)

- Purpose:

- System to recover NPAs from the books of secured lenders and unlock value from distressed assets.

- Licensing:

- Licensed by RBI.

- Empowered by:

- SARFAESI Act, 2002.

- Functions:

- Acquisition of financial assets

- Takeover or change of management

- Rescheduling debts

- Enforcement of security interest

- Settling dues with borrowers

- 2011 Amendment: Convert debt into equity

- Funding for ARCs:

- Raised via Security Receipts (SRs).

- Only Qualified Institutional Buyers (QIBs) can purchase SRs (e.g., scheduled banks, mutual funds, venture capital, insurance companies, pension funds).

- Foreign Investment:

- 100% FDI allowed through the automatic route.

8. Sustainable Structuring of Stressed Assets (S4A)

- Conditions:

- The project must be operational and generating revenue.

- Total loan must exceed ₹500 crore.

- 50% of the loan should be sustainable.

9. Indradhanush Scheme

- Appointment of Executives:

- Bring private sector executives into public banks.

- Empowerment:

- Provide autonomy and flexibility to banks.

- Framework:

- Key performance indicators for banks.

- Professionalization and Depoliticization:

- Professionalize the appointment process for bank executives (BBB framework).

10. Foreign Direct Investment (FDI) in Banks

- PSBs:

- FDI limit is 20%.

- Private Banks:

- FDI limit is 74%.

- Up to 49% is automatic, beyond that, approval is required.

- Voting Rights Cap:

- Voting rights are capped at 10% for national interest.

11. Public Sector Asset Rehabilitation Agency (Bad Bank)

- Concept:

- Based on successful models in East Asian countries.

- Special Purpose Vehicle (SPV) for handling distressed assets.

- Funding Sources:

- Government Bonds

- Shares

- Disinvestment funds from PSUs

- Windfall gains from RBI (e.g., from demonetization)

- Government Shareholding:

- Government share cannot exceed 49%.

- Debt to Equity Ratio:

- Debt financing is used in combination with equity funding.

12. Recapitalization

- Purpose:

- To infuse capital into banks, particularly PSBs, to ensure compliance with regulatory norms (e.g., Basel III).

- How recapitalization works:

- Government infusion of capital to strengthen bank balance sheets.

1. Bad Loans

- Standard Asset:

- A performing asset that is not overdue.

- Substandard Asset (NPA):

- Asset for which neither interest nor principal has been paid for a specified period.

- Classification Timeline:

- Special Mention Account (SMA): < 12 months

- Substandard Asset: 90 days

- Doubtful Asset (DA1): After 1 year

- DA2: 1–3 years

- DA3: Beyond 3 years

- Stressed Asset:

- Assets showing weaknesses but still classified as standard. RBI allows restructuring.

- Types of NPA:

- Overdraft and cash credit accounts out of order for >90 days.

- Agricultural advances overdue:

- 2 crop seasons for short-duration crops.

- 1 crop season for long-duration crops.

- Bills overdue >90 days.

- Expected payments overdue for >90 days.

- Non-submission of stock statements for 3 consecutive quarters in cash credit facilities.

2. Foreclosure and Securitization

- Foreclosure:

- Lender takes over mortgaged property when the borrower defaults.

- Securitization:

- Pooling a group of loans or mortgages and selling securities backed by these assets.

3. Prudential Norms

- Purpose:

- Reflect the true position of the bank’s loan portfolio.

- Prevent portfolio deterioration.

- Focus Areas:

- Income recognition.

- Asset classification.

- Provisioning for NPAs.

- Capital adequacy norms (CRAR).

4. Write-Off, Write-Down, Haircut

- Write-Off:

- Automatic once the asset crosses DA3 class.

- Refers to NPAs that cannot be recovered without legal or recovery processes.

- Haircut:

- Measure to adjust capital adequacy.

- Asset value reduced to reflect partial recovery.

- Write-Down:

- Partial write-off of a loan decided by the lender.

5. Priority Sector Lending (PSL)

- Categories:

- Agriculture.

- Micro, Small, and Medium Enterprises (MSMEs).

- Export credit.

- Education.

- Affordable housing (loans ≤ ₹10 lakh).

- Social infrastructure.

- Renewable energy (loans ≤ ₹15 crore; hydro projects <25 MW).

- Others (e.g., road and water transport, retail trade).

- Weaker Sections:

- Distressed farmers indebted to non-institutional creditors.

- Overdrafts in Jan Dhan accounts <₹10,000.

- Distressed individuals indebted to non-institutional creditors (loans ≤ ₹10 lakh).

- Targets:

- Domestic Scheduled Commercial Banks: 40% of Adjusted Net Bank Credit (ANBC).

- Regional Rural Banks (RRBs): 75% of ANBC.

- Foreign Banks: 36% of ANBC.

- Sub-Targets for Scheduled Commercial Banks: Category Sub-Target Agriculture 18% Micro Enterprises 7.5% Weaker Sections 10% (or 25% of PSL, whichever is higher).

- Shortfall in PSL Targets:

- Shortfalls must be deposited with NABARD’s Rural Infrastructure Development Fund (RIDF).

- NABARD allocates these funds to state governments for rural development activities.